Rethinking Today's High Housing Costs

Michael Anderson

July 19th, 2021

How incorporating self-storage in your housing budget gets you more bang for your buck.

In all my time spent studying real estate investments, I have served three formidable mistresses.

In my youth, my family was heavily involved in the business of entry level home building. Put plainly, this is the first house you buy when you decide it is time to be a homeowner as opposed to just a renting. My father and uncle had me do everything. My first job occurred over the summers during middle school, shoveling and moving dirt with a wheelbarrow. Progressing to my summer job in high school of swinging a hammer and helping build the houses framework. Then transitioning to working in the sales office, my college and first ‘wear a suit to work’ job. Finally, graduating to project management in my first full time career post college graduation. This was my first mistress: delivering hundreds of homes to new home buyers.

Eventually, I developed a severe case of career wonder lust and several years later I left the family business. Eventually I found myself in the arms of my second mistress, multifamily property investments. I started a real estate investment firm of my own in 1991 and by the time I sold it in 2018, with the intention of retiring, it had grown just shy of a billion dollars in assets. This was my second mistress, and I still own many of these property assets today.

It took me awhile to realize that I did not know how to retire. Perhaps, I did not want to retire. So, I found my third mistress, self-storage. The funny thing is, self-storage when you think about it, is kind of an extension of my other two mistresses, housing, and multifamily properties. Housing/renting is the necessity of a roof over my head and protection for the stuff in my daily life from the outer elements. Storage is just an extension of the necessity of protecting the stuff that is an extension of my life. The interplay between housing and storing is what stirred me to write this post.

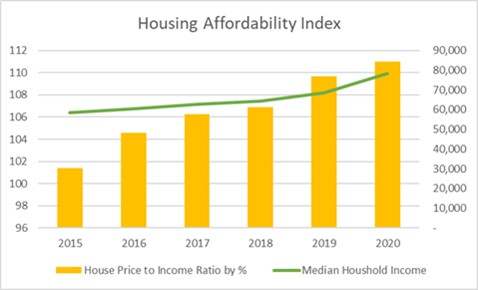

Currently home ownership still represents the best economic value for protecting what is important in our lives. Although, as Bob Dylan once wrote “The Times They Are A Changin”. Today home ownership is becoming less affordable and homes, including the lots they are built on, are ‘downsizing’ to meet affordability requirements (see: Figure 1. Housing Affordability Index).

Home Affordability, is still a bargain. For now... (see: Figure 1. Housing Affordability Index) Figure 1

{kind=link}

Description: In the third quarter of 2020, the house price to income ratio in the U.S. amounted to 109.31 percent. This ratio was calculated by dividing nominal house prices by nominal disposable income per head. The ratio was gradually increasing from 2015 to the first quarter of 2020, which means that house prices were rising faster than income. Due to covid 19, adjustment was made to the 2020 on the OECD cost index to reflect debt forbearance. For clarity, I included the median household income to the graph. The median household income depicts all income of households, including the income of the householder and all other individuals aged 15 years or older living in the household. Source: US Census Bureau.

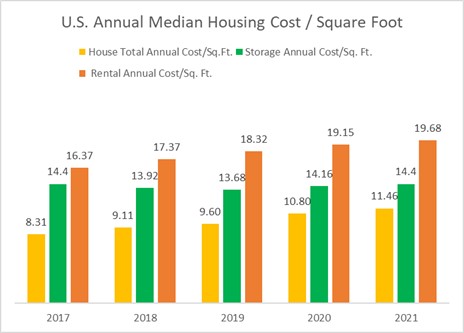

Looking comparatively at the housing field. (see: Figure 2. Housing Annual Cost/Sq. Ft., U.S. Rental rates) Figure 2

{kind=link}

When you compare the cost of keeping a roof over the things in your life you really get a sense what a bargain home ownership has been on an annual cost per square foot basis (see, Figure 2. Housing Annual Cost/Sq. Ft.). You also notice how quickly it is losing ground to the more stable cost of commercial storage. When calculating the cost of home ownership, I used median house prices divided by the median house size to get the median price per square foot. I then amortized the cost at the then current mortgage rate and then added in estimated taxes and annual maintenance costs. This provides a more accurate representation of cost of home ownership. It also represents a more of an ‘apples to apples’ comparison approach when evaluating home ownership to renting.

When it comes to renting there is no question that storage is a far better option for the ancillary items of our lives rather than renting a larger unit. I have found there is many reasons why people rent rather than own, and this discussion is for another blog I hope to write soon. Briefly, some of the key reasons are affordability, credit and more importantly for many these days, is a live style consideration. Many renters simply do not want to be locked down to a place, mortgage or the maintenance issues related to ownership.

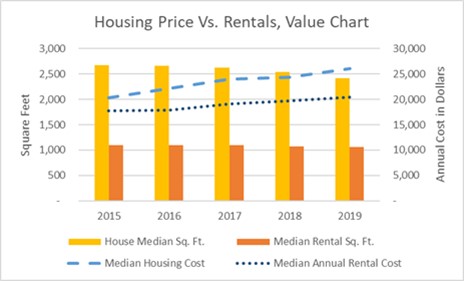

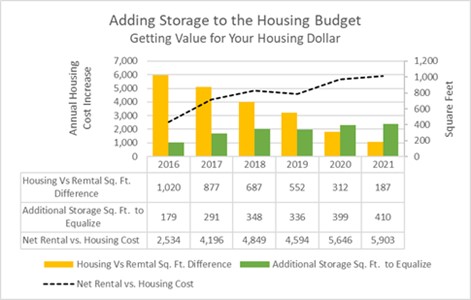

Renting carching up to homeownership on the value scale. (see: Figure 3. Homeownership vs. Renting) Figure 3

{kind=link}

Figure 3. Homeownership Vs. Renting Illustrates how renting is closing the gap to homeownership when it comes to value. Although apartments rents are rising the square footage of the median rental unit remains relatively constant. Median home sizes on the other hand are getting smaller and prices are rising at a faster rate. Whatever the case, here’s the deal; your house or apartment is where your life takes place. It is where you entertain, relax, dine, sleep and so much more. Your life’s stage, the place you reside, is the most valuable space of all and it is becoming less affordable and therefor smaller. It is also, for most of us, the biggest portion of our monthly budget. All while continually getting smaller and more expensive.

Once you have made a commitment, either by lease in the case of a rental space or a purchase in the case of a mortgage, we are obligated to that space. You add a dog, child, boat, a work from home job, whatever, it all must fit in that space. At least for the time being. I kind of think of housing space as hard sided luggage, it fits what it fits and makes no adjustment relative to contents or the traveler’s needs. When you add storage to your housing consideration it is more like soft sided luggage. With its short-term rental commitments and variety of sizes it can adjust relative to its owner’s content needs.

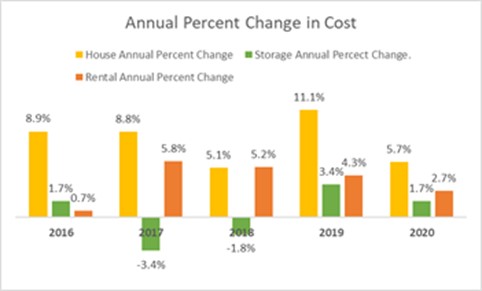

Lowering housing cost with the flexibility and stability of storage. (see: Figure 4. Year over year percent change in cost) Figure 4

{kind=link}

Although storage costs are a little bit of a roller coaster ride over the past five years, they tend to stay constant when compared to the steady increase in home and apartments. See Figure 4. Year over year percent change in cost.

If you are renting the path is clear. Because this is the most expensive housing space coming in at a median price north of $19.50/sq. ft./ yr. you spend your budget on living space and store as little as possible in your rental. Storage is a much better bet for the extra stuff in your life, coming in at a median price of around $14.40/sq. ft./ yr. That roughly comes out to a $5/sq. ft./ yr. difference. NICE!

Why future homeowners should plan on self-storage as part of their budget. (

see: Figure 5. Renting catching owning in value proposition. As cost of renting and owning rise, storage gets a bigger bang for the buck) Figure 5

{kind=link}

When it comes to home ownership the equation is a bit murkier. The nature of home ownership is one of more permanency. According to a January 2020 blog post by Nadia Evangelou, a Senior Economist & Director of Forecasting at the National Association of Realtors, the median length of ownership in the U.S. is now 13 years. Going back to my hard sided luggage metaphor. 13-year ownership of the same house is a little like taking an extended vacation to a foreign country with a hard sided bag that was full when you left. The reason it was full was due to the affordability issue at the time of departure. This is certainly the case today with smaller homes and smaller, deed restricted lots.

Far sighted buyers may look to by homes with future finish able spaces like basements or bonus space over the garage. That is a little like a hard sided bag that has an expandable, soft center, you know the type of bag I’m talking about. Clever but a little more spendy. However, in the 13-year journey you eventually gather more than your bag can carry. That is where the far more consistently priced storage space can extend the time in your current home (see. Figure 4. Year over year percent change in cost.). Going back to the baggage metaphor, many of us have learned a little trick in our travels, pack a second, lightweight, soft sided bag in your hard sided bag. It adds extraordinarily little weight, is perfect for clothes, and other non-fragile items. Keep the fragile items and keepsakes in the hard sided bag while the soft bag allows you to travel light, for longer. Self-storage works the same way in your housing budget. It can expand or contract based on short term rental agreements, light on the budget and stores items not needed on a daily basis.

Extending the tenancy in your home this way could save you tens of thousands of dollars in inflationary housing cost when all you may have needed is a little less “stuff space” and a little more “people space”. This concept can be so important for families with school age children when their location stability is vitally important. Attributes to think about are, first location considerations like quality schools, local crime rates, and community services. Next, look for home specific value in its expansion potential such as unfinished spaces, larger lot size and the homes design flexibility (budget permitting). Saving tens of thousands of dollars; EVEN BETTER.

Final thought, no need to buy and sell to realize your homes appreciation, If the housing market is appreciating, which it usually does, then the home you’re in is building equity with a lower cost basis and less risk. If you really want to realize the equity gain and add a little risk, I suggest you refinance at today’s lower rates. Take the proceeds, which are most likely not taxable and reinvest that money. May I suggest self-storage and/or multifamily. They have been exceptionally good to me. I’ll write you another how-to blog on the topic if you’re interested.

GreenFill Storage Blog